CLEAR

Prevent fraud, detect risk, and investigate crime with powerful online investigation software

Bring key content together to connect the facts and provide intelligent analytics through one solution with CLEAR, a public records technology tool

Providing businesses and professionals with the data and connections that deliver results

Make confident decisions with access to CLEAR's current and trusted data

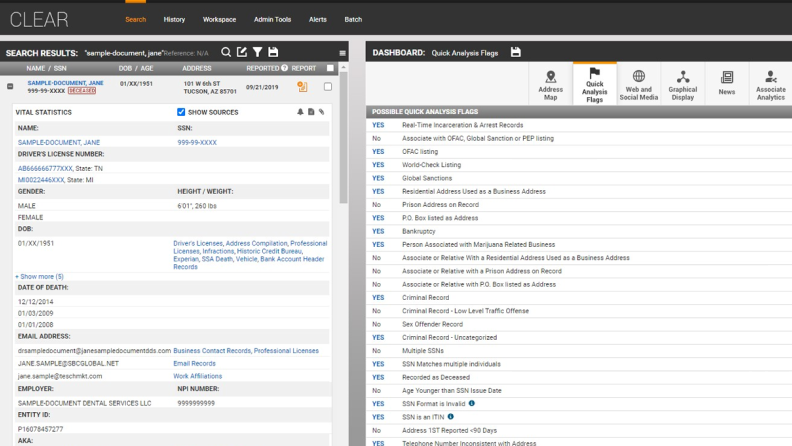

Accelerate investigations confidently through a vast collection of public and proprietary records with CLEAR's online investigation software. Access exclusive data feeds, quality domestic data, and incarceration records with source transparency and frequent updates, all in a single platform.

Have questions?

Contact a representative

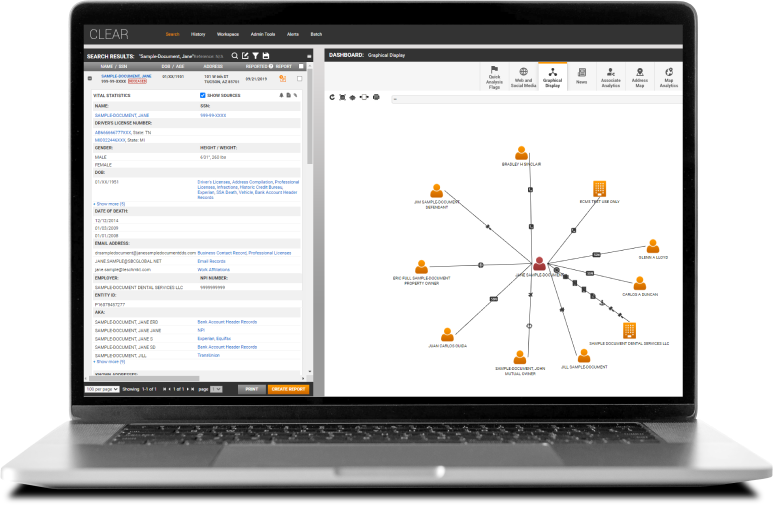

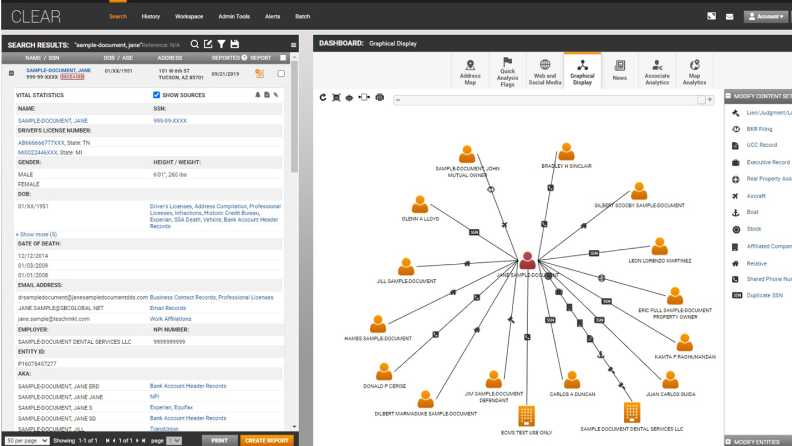

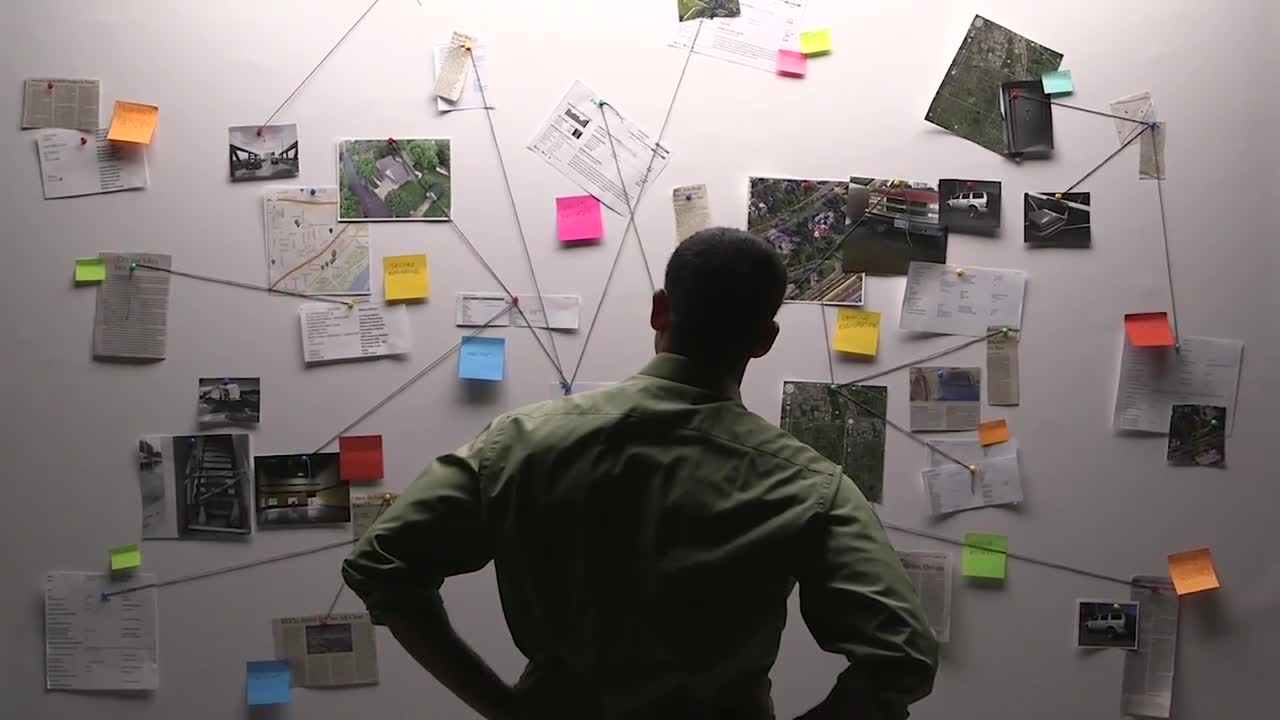

Easily identify and analyze your subject's connections

Locate hard-to-find information and quickly identify potential concerns and connections to determine if further analysis is needed. Easily connect information about people, businesses, assets, affiliations, and other vital content.

Have questions?

Contact a representative

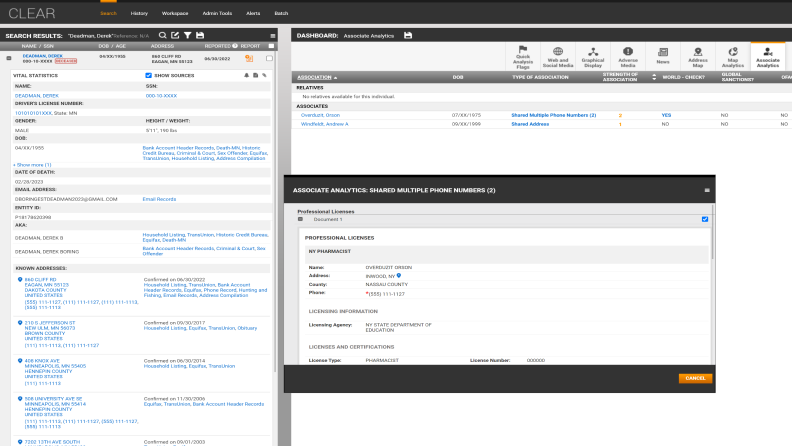

Access advanced analytics powered by AI machine learning

Reduce the amount of searching with CLEAR’s powerful entity resolution capabilities. Close investigations faster by overcoming partial and incomplete data and scoring relationships by confidence level.

Have questions?

Contact a representative

CLEAR powers corporate and government professionals throughout their investigation workflows

Financial services

Utilize CLEAR's investigation software for financial services to conduct enhanced due diligence (EDD) on clients and business partners. Review comprehensive information to help with your investigation process.

Law enforcement

Quickly identify victims and persons of interest through current and historical content. Simplify your search, view connections, and zero in on the insights most important to your investigation.

Retail

Improve your validation process and gain insights to easily identify, understand, and resolve fraudulent transactions.

Child and family services

Locate individuals who are not making mandatory payments and increase the amount collected in unpaid child support by closing more cases.

Manufacturing

Perform know-your-vendor processes, supply chain risk management, and due diligence on new and existing business partners to safeguard your company from potential risky and fraudulent vendors.

School districts

Utilize CLEAR's public records and batching capabilities to complete residency verification for your district efficiently. Access extensive public records to complete family document validation and speed up deeper investigations.

Embrace the full capabilities of CLEAR

See CLEAR in action

See how CLEAR powers professionals to complete investigations quickly and efficiently.

See why professionals choose CLEAR investigative solutions to streamline their investigation workflow

"CLEAR is like the picture on the puzzle box. It gives me that clear picture I need to put all the pieces together."

Samantha Eriks

Investigator, Child Support Division, Prosecutor’s Office, Lake County, Indiana

“When I conduct an investigation, and I’ve been doing this for over 30 years, I always start with CLEAR.”

Theresa Mack

Senior Manager of Investigations, Cendrowski Corporate Advisors

"CLEAR is what gave us the starting point. All we really had was that email, an IP address, and an open WI-FI at the hospital which anybody could use."

John Peirce

Davis County Detective

Questions about CLEAR? We're here to support you.

888-728-7677

Call us or submit your email and a sales representative will contact you within one business day.

CLEAR support

Already a customer?

Access to these tools is limited to authorized, vetted professionals.

Thomson Reuters is not a consumer reporting agency and none of its services or the data contained therein constitute a “consumer report” as such term is defined in the Federal Fair Credit Reporting Act (FCRA), 15 U.S.C. sec. 1681 et seq. The data provided to you may not be used as a factor in consumer debt collection decisioning; establishing a consumer’s eligibility for credit, insurance, employment, government benefits, or housing; or for any other purpose authorized under the FCRA. By accessing one of our services, you agree not to use the service or data for any purpose authorized under the FCRA or in relation to taking an adverse action relating to a consumer application.